Trading

Content focused on trading across financial markets, covering trading approaches, risk management, order execution, and price behavior

Market makers without myths: algorithms, volume, and spread control

Why order book depth disappears when it’s needed most

How to Check for Altseason After a BTC.D Drop

A BTC.D drop is a cue to check Total3 and ALT/BTC, not a ready-made signal of an alt rally.

Why Liquidation Doesn’t Match the Chart Price

How reference prices replace the last trade in liquidation

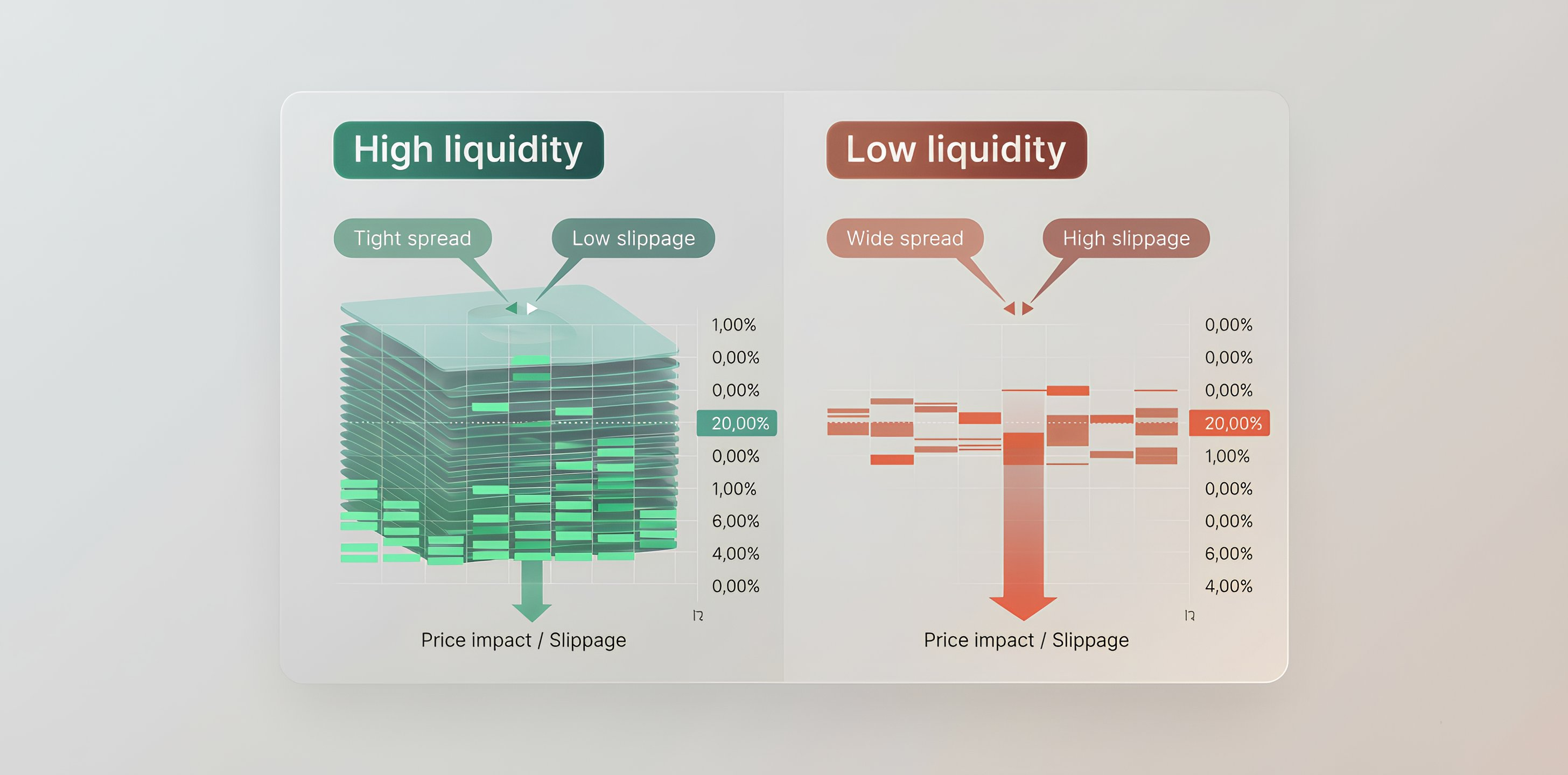

Market liquidity: what this term means

Liquidity definition, its sources, and concept limits—no practical algorithms

Futures liquidation deficit: what happens in a price gap

A shortfall in settlement appears when a liquidation executes worse than the bankruptcy price.

Why news doesn’t break the nearest order book levels

Price stays in a range if the first market orders fit into the depth at the best bid/ask

How to set up VWAP and TWAP so slices don’t go deeper into the order book

Quick pre-run check: set slice size and a limit so the order doesn’t move deeper into the order book

VWAP and TWAP in trading: how to execute large orders without unnecessary slippage

VWAP and TWAP help execute large orders without moving price or revealing intent early

Liquidation deficit in futures: why execution moves below the bankruptcy price

A negative balance appears when liquidation executes below the bankruptcy price because of gaps and slippage

Why liquidation does not match the chart price

How a calculated risk price replaces the last trade in the liquidation trigger

Open interest in crypto: how to read the market, not illusions

How open interest tracks contract count and liquidation risk when leverage is used

Quant Trader: Who They Are, What They Do, and How to Become One

A complete breakdown of a profession that combines mathematics, programming, and algorithmic trading

Frameworks for Algorithmic Trading: Where to Start When Building a First Strategy

A practical guide to choosing a framework and launching a first algorithmic trading strategy

Why price can jerk after a crypto ETF launch

How the T+1 lag, share turnover, and collateral operations create price jolts

How to set up VWAP and TWAP so the order does not move deeper into the order book

VWAP/TWAP order book setup: slice size, interval, and limit price without excessive depth pressure

Why a drop in BTC dominance does not confirm altseason on its own

BTC share can fall through stablecoins, narrow growth, or Bitcoin weakness, not broad altcoin demand

Market liquidity: what this term means

Explaining liquidity through spread, slippage, order books, and DeFi pools

Why news does not break order book levels

Even major news may leave price range-bound when expectations formed before the release

BTC dominance: what Bitcoin dominance and the BTC.D index show

How Bitcoin’s share of market capitalization helps read rotation, risks, and crypto market structure

Insurance Fund on crypto exchanges: who covers losses during a price gap

Insurance funds in derivatives, negative liquidation, and why protection can sometimes end abruptly